UK flash PMI signals accelerating economic recovery but price pressures surge higher

Early PMI survey data for April indicate that the UK economy's recovery from recession last year continued to gain momentum. Improved growth in the service sector offset a renewed downturn in manufacturing to propel overall business growth to the fastest for nearly a year, indicating that GDP is rising at a quarterly rate of 0.4% after a 0.3% gain in the first quarter.

The upturn encouraged firms to take on workers in increased numbers which, alongside April's rise in the National Living Wage, drove cost pressures sharply higher. Although selling price inflation cooled slightly, the upturn in costs alongside solid demand suggests firms may seek to raise prices in the coming months.

While the improving economic recovery picture is welcome news, the upward pressure on inflation will add to concerns that a sustainable path to below target inflation has not yet been achieved.

Economic growth at 11-month high

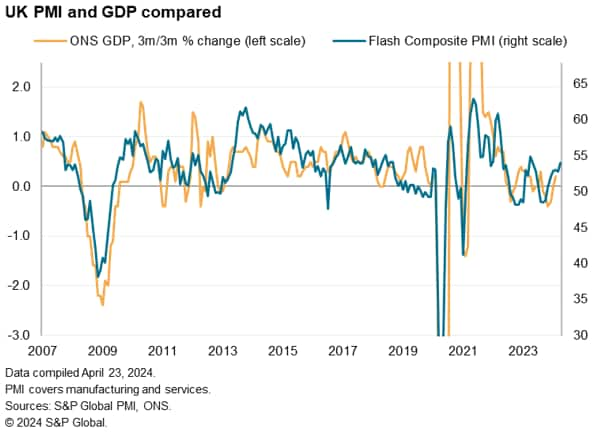

Business activity growth accelerated to an 11-month high in April, according to early PMI survey indications. The headline economic growth indicator from the flash PMI surveys, the seasonally adjusted S&P Global UK Composite Output Index, registered 54.0 in April against 52.8 in March. The latest reading signals a sixth successive monthly expansion of output, with the rate of growth rising to the highest since May of last year. April's expansion is broadly consistent with GDP growing at a quarterly rate of almost 0.4% at the start of the second quarter, building further on the robust 0.25% gain signalled by the PMI in the first quarter.

The survey data therefore indicate that the UK economy continues to pull out of the technical recession seen late last year, recovering to register solid growth.

The latest official GDP are also showing signs of the recession having ended, with monthly GDP having risen for a second successive month in February. First quarter GDP data are so far also running 0.3% above the fourth quarter of last year, in line with the PMI signal.

Services-driven growth while manufacturing stabilises

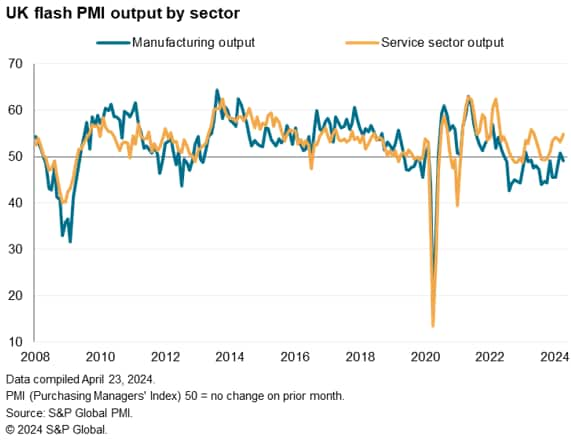

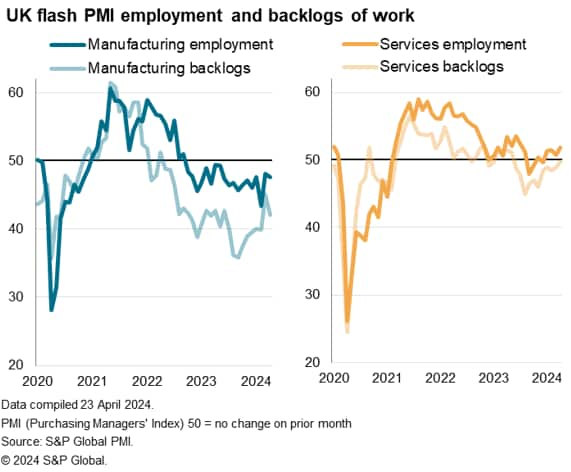

April's improvement was driven by the service sector, which as a whole grew at the strongest rate seen for 11 months. Trends varied markedly within services, however. The strongest performing sector was financial services, followed by tech/IT, but only a modest gain was recorded for business services, and other sectors such as transport and hospitality reported falling output.

Falling output was also seen in the manufacturing sector, reversing the modest return to growth in March (which had seen the first increase in factory output for just over a year).

Elevated optimism - in the service sector

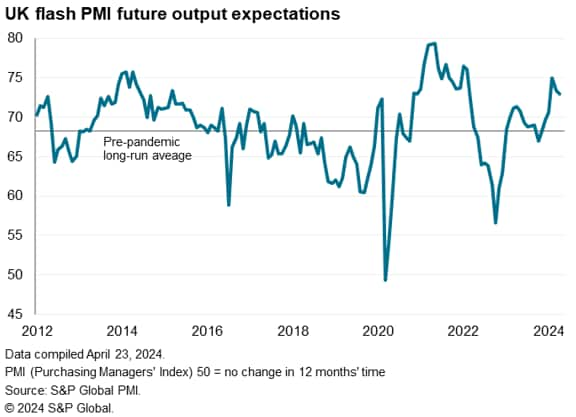

The improved business growth in April was accompanied by continued elevated levels of optimism about the 12-month outlook. Business expectations about the year ahead fell further from February's two-year high but remained well above the survey's long-run average, in part reflecting an accelerated rate of increase of new orders, which rose at the sharpest pace for 11 months.

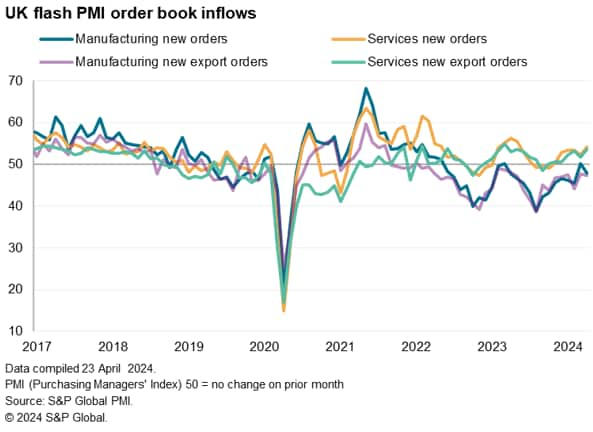

However, sector variations were again evident by sector in terms of outlooks and order books. Manufacturing future sentiment fell to a four-month low as new orders contracted after a marginal gain in March, linked largely to lower exports, which have now fallen continually for 27 months. In contrast, service sector future sentiment lifted higher, amid increased rates of growth of both new business and exports.

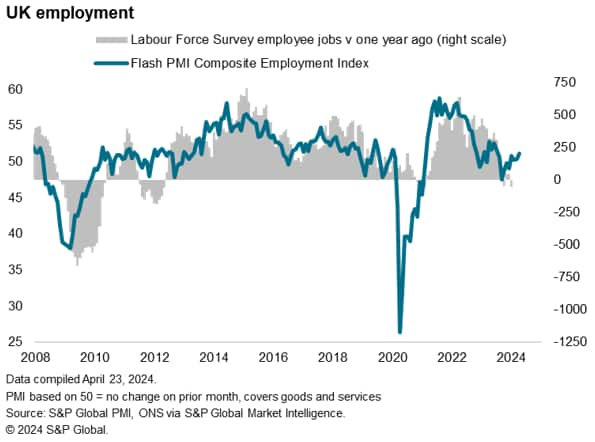

Hiring picks up

Hiring picked up on the back of the improved demand situation and increased workloads, albeit with gains limited to the service sector. Measured overall, employment rose for a fourth successive month in April, rising at the fastest rate for nine months. However, a steeper rate of jobs growth in the service sector was countered by a slight acceleration in the rate of factory job culling. While service sector payrolls have now risen for four successive months, manufacturing headcounts have fallen continually over the past 19 months.

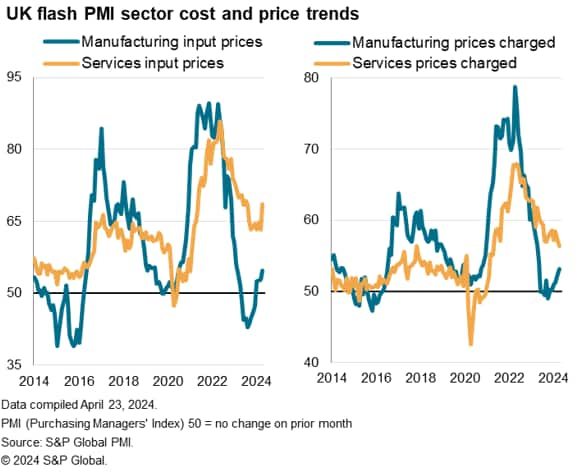

Selling price inflation cools despite National Living Wage adding to price pressures

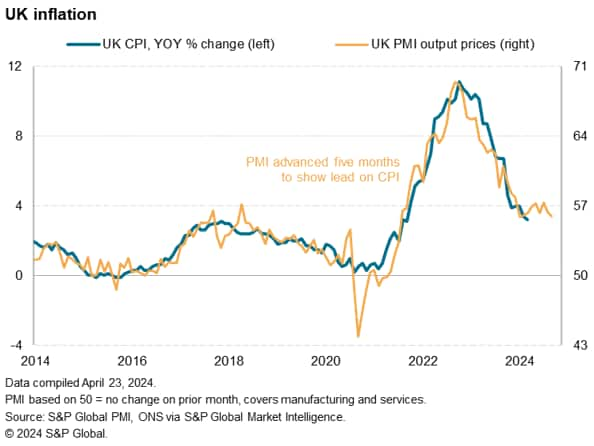

Average selling prices charged for goods and services rose in April at the slowest rate since last August, and the joint-slowest rate since February 2021. The latest data nevertheless remain elevated by historical standards, and broadly consistent with inflation (headline CPI) running close to 4%. There were also some notable details beneath the headline selling price number, which hint at some possible renewed near-term upward pressure on prices.

Encouragingly, service sector selling price inflation, which has proven to be the most stubborn aspect of inflation in recent months, slowed in April to a three-year low. However, service sector input cost inflation jumped higher to hit a nine-month high, buoyed in particular by higher wages.

It should be noted that the April PMI data include the impact of the introduction of the latest National Living Wage (NLW) increase. Effective from 1st April, the recommended wage increased from £10.42 to £11.44, a rise of 9.8%.

Manufacturers' selling prices meanwhile rose at the sharpest pace since last May, as firms passed higher costs on to customers. Manufacturing costs grew at the fastest rate since February 2023, having now risen for four consecutive months after eight months of continual decline.

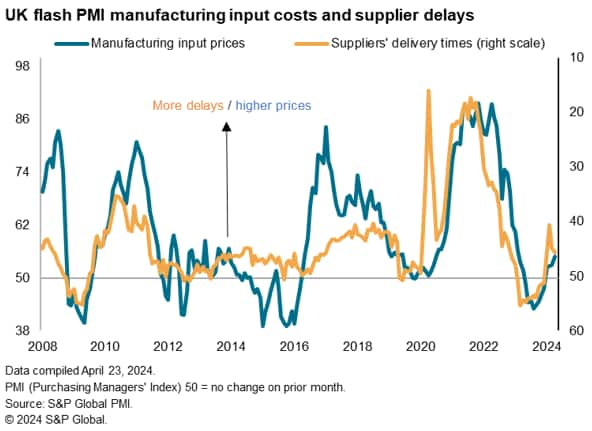

In manufacturing, an additional cost driver was renewed raw material supply shortages. April saw average supplier delivery times lengthen for a fourth successive month, with delays again often linked to Red Sea-related shipping disruptions. Longer lead-times tend to be associated with higher prices as a reflection of demand exceeding near-term supply, though the need to re-route ships around Africa has also directly raised shipping costs so far this year.

Average input costs across goods and services consequently rose sharply in April, the rate of inflation surging to the highest recorded since last May. The 4.8 point increase in the Composite Input Cost index was the largest recorded since October 2021, and represents a hike in costs that companies may seek to pass on to some degree to customers in the coming weeks or months.

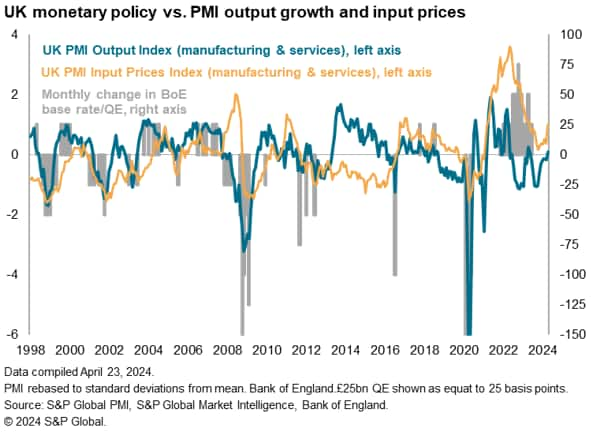

Not a rate cutting environment

The latest PMI data follow growing expectations that the Bank of England may start cutting interest rates as soon as June. However, the upturn in the pace of economic growth signalled by the PMI, and the upsurge in firms' cost pressures, suggest that business conditions are more consistent with rate hikes rather than rate cuts. Both the composite flash PMI output index and input cost index are above their long run averages and rising.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2024, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.