Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Feb 11, 2021

Reinventing the refinery through the energy transition and refining-petrochemical integration

As the world moves away from fossil-based fuels to renewable energy, refiners will continue to face the realities of the ongoing energy transition. With an increased focus on climate change concerns and sustainability, shifting consumer habits will impact the refining industry in an unprecedented manner. Emphasis on reducing the use of fossil fuels and the carbon footprint of everyday human activities will cause a peak in fuel consumption - starting with gasoline, then other fuels, and finally crude oil demand.

At the same time, chemical derivatives demand is forecast to continue to grow as the population increases and living standards improve across the world. Some believe the ongoing COVID-19 pandemic could set the stage for a future world with lower demand for transportation fuels and higher demand for petrochemical feedstocks. This shift would be the result of less commuting to the office and stable consumption of non-durable plastics. It is clear that an option for lost fuels demand is transforming those hydrocarbons into petrochemical feedstocks, which can be achieved through the use of different technologies - some already available and others still under development.

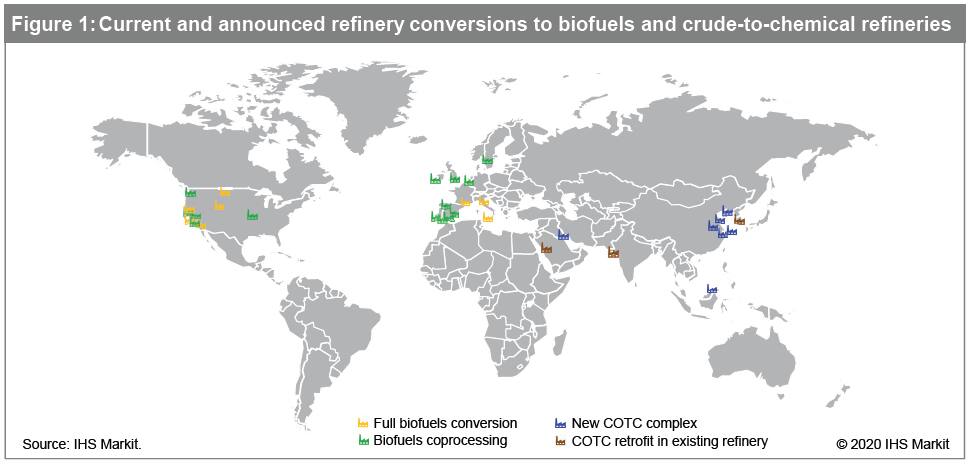

There are several different options for the refining industry, and no one-size-fits-all solution for the declining fuels demand issue. In recent years, refineries have been shut down, converted to logistics terminals or converted - partially or totally - to biofuels (see Figure 1). There has also been investment in crude oil-to-chemicals (COTC) facilities.

Although switching refining yields to petrochemicals may seem like an obvious choice to increase processing margins and achieve growth, the reality is that the scale of the refining and petrochemicals markets differs widely. Investments in increasing petrochemical production in refi neries could easily swamp product markets. Furthermore, these investments require significant capital commitment and scale, which may be feasible only in certain locations.

Growth and decline

IHS Markit energy scenarios provide a framework for understanding

the energy transition under different sets of assumptions. The base

case, the Rivalry scenario, considers emerging trends, albeit at a

reduced rate of change. This means a slower pace of adoption of

electric vehicles, among other trends, and oil demand peaking in

the 2030s. The Autonomy scenario assumes a quicker adoption of

electric vehicles and other disruptive technologies that impact

refined-product demand. Both scenarios forecast a peak in

refined-product demand, but let's discuss the base case. In

contrast, chemicals demand is growing continuously and is not

forecast to peak anytime through the forecasting period. Population

growth is a key driver for petrochemicals demand. This is due to

the increase in global population, forecast to surpass 9 billion by

2040, and the per-capita consumption of petrochemical derivatives,

as the standard of living increases with economical growth and

development. The great variety of end uses for petrochemical

products - durable and non-durable, technology, medical, packaging,

automotive, construction, and so many other applications - support

robust growth in different scenarios.

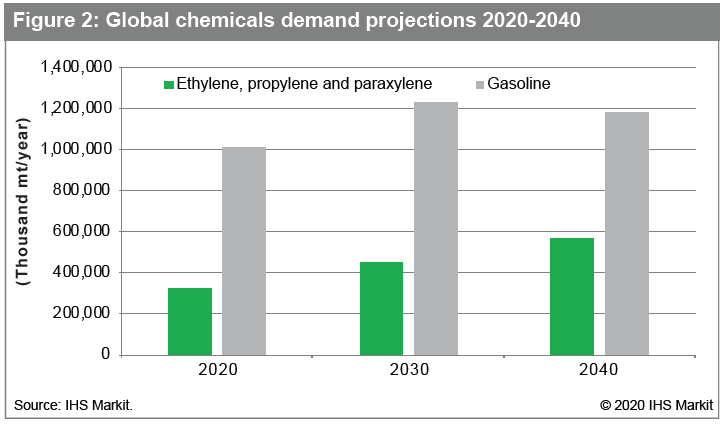

Nevertheless, there is still the issue of scale. While crude oil demand is forecast to peak and petrochemical demand is not, petrochemical demand occurs at a much smaller scale. Figure 2 summarizes ethylene, propylene, and paraxylene demand, as those are the building blocks for the main drivers of chemicals growth. From 2020 to 2030, those chemicals will grow 39%, while gasoline is forecast to grow only 22%. Nevertheless, in absolute terms, gasoline demand still outpaces those chemicals, growing 218 million metric tons per year against 126 million metric tons per year of petrochemicals. In the 2030s, the situation reverses, with gasoline demand starting to decrease while chemicals demand grows robustly. Chemical products demand grows 25%, or 115 million metric tons, while gasoline demand is forecast to decrease 4%, or almost 50 million metric tons, in the same period.

Winners and losers

In order to meet future petrochemicals demand, naphtha yields in

refineries will increase from the current 12% to 19% by 2040 -

growth driven by both rising demand and slower natural gas liquids

(NGL) supply growth. As gasoline demand decreases, less of the

"by-product" naphtha will be available. Refineries will be

reconfigured to increase naphtha and other petrochemical products

supply in two ways:

- New greenfield projects designed with petrochemical yields from +40%, such as the current COTC project recently built in Asia

- Brownfield investments in existing refineries with technologies that enable increased petrochemicals production, either by retrofitting existing units, such as typical FCCs and hydrocrackers, or by using newer technologies being developed for repurposing existing refineries

Independent refining and petrochemicals

investments

To determine how these investments will change the shape of the

refining industry globally, it is important to look at not only

regional demand and the availability of feedstocks and existing

assets, but also at the economics of the new investments -

especially the different capital requirements, operational

synergies, and freights required by different alternatives. It is

clear that opportunities exist for some but not all market players.

IHS Markit has continued to research the topics:

- The Process Economics Program includes several reports analyzing current COTC technologies and trends (PEP 303, 303A, 303B).

- The Refinery Costs and Margins Analytics (RCMA) incorporates integrated petrochemical production into its economic analysis of individual refineries, both currently operating as well as for announced projects.

- The Light & Heavy Naphtha Service consolidates the refining and chemicals long-term supply and demand balances, providing a global integrated picture for naphtha.

- The demand scenarios for energy and refined products address the impact of different trends in consumer behavior for fuels and refined products, in IHS Markit scenarios named "Rivalry," "Autonomy," and "Vertigo."

- The Changing Course Strategic Report analyzes the impact of the same consumer behavior trends in plastics and chemicals consumption and recycling.

Still unclear is how the refining industry will adapt to these changing trends. How much capacity will be rationalized? How much will be repurposed? And how much will be integrated into petrochemicals? Furthermore, out of the latter, how many will be new COTC complexes and how many will be retrofitted existing refining capacity? In which regions and countries will investments be made?

Those questions will be explored and addressed in a new Strategic Report, to be published in the first half of 2021, that will model new capacities for refining and petrochemical integration. The report will consider how much capacity will be added, where it will be added, and whether it will be new capacities or brownfield investments.

For more insight into Energy and Climate scenarios, visit ihsmarkit.com/energyclimatescenarios

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fssl.ihsmarkit.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fenergy-transition-and-petchem-integration.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fssl.ihsmarkit.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fenergy-transition-and-petchem-integration.html&text=Reinventing+the+refinery+through+the+energy+transition+and+refining-petrochemical+integration+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fssl.ihsmarkit.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fenergy-transition-and-petchem-integration.html","enabled":true},{"name":"email","url":"?subject=Reinventing the refinery through the energy transition and refining-petrochemical integration | S&P Global &body=http%3a%2f%2fssl.ihsmarkit.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fenergy-transition-and-petchem-integration.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Reinventing+the+refinery+through+the+energy+transition+and+refining-petrochemical+integration+%7c+S%26P+Global+ http%3a%2f%2fssl.ihsmarkit.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fenergy-transition-and-petchem-integration.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}